The public sector spending on Cloud services through G-Cloud and DOS on the Digital Marketplace for the financial year 2022/23 has now been published by Crown Commercial Service (“CCS”) and here, our Strategic Adviser Lindsay has been looking through the numbers and asking what it tells us about this £4.4Bn market.

Summary

- Quick definition of the statistics we are following after changes

- DOS has another strong year

- What’s been happening on the demand side – customer base

- Supply side, plus ça change, SMEs: don’t quit! Think Buyability™

- Professional Services – is this a racket?

- Software – first decline in 11 years

- Hosting – create a monopoly in haste, repent at leisure

Necessary but boring

2022/23 was a year of many changes, in Downing St., Whitehall, Holyrood and just a tad more prosaically, for those of us interested in the Digital Marketplace, several changes in the structure and composition of the frameworks that we have got to know as G-Cloud and DOS. To make the statistics as backwardly compatible as possible, so trends over time have meaning, we first need to define which frameworks and Lots we are tracking in the data and will track going forwards. In combination, I will refer to these as the Digital Marketplace:

Included in DOS:

Digital Outcomes & Specialists 1 – 5

Digital Outcomes 6

Digital Specialists & Programmes

Included in G-Cloud

G-Cloud 1 – 13 Support, Software & Hosting (i.e., Not including Lot 4 for End-to-end Cloud Services.)

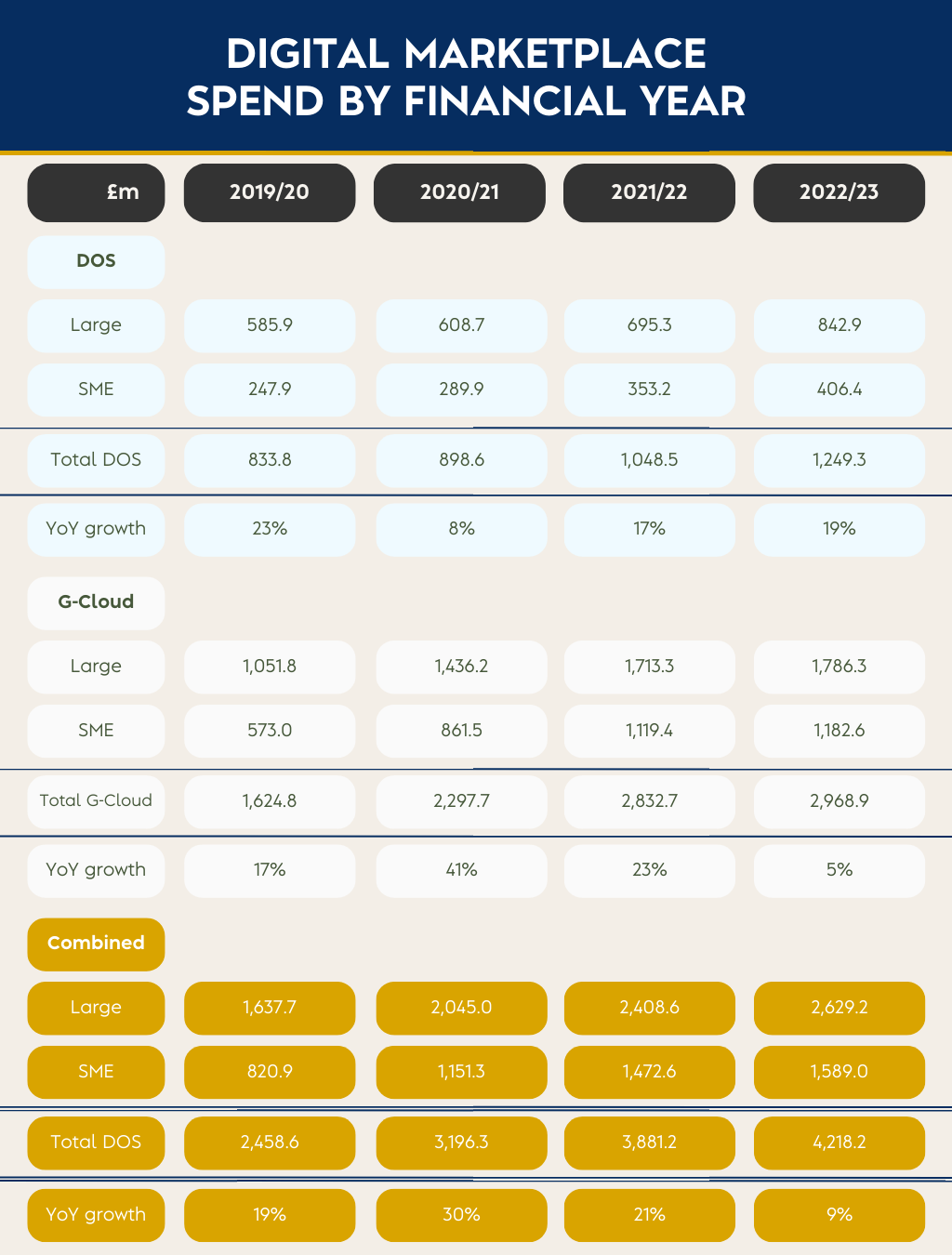

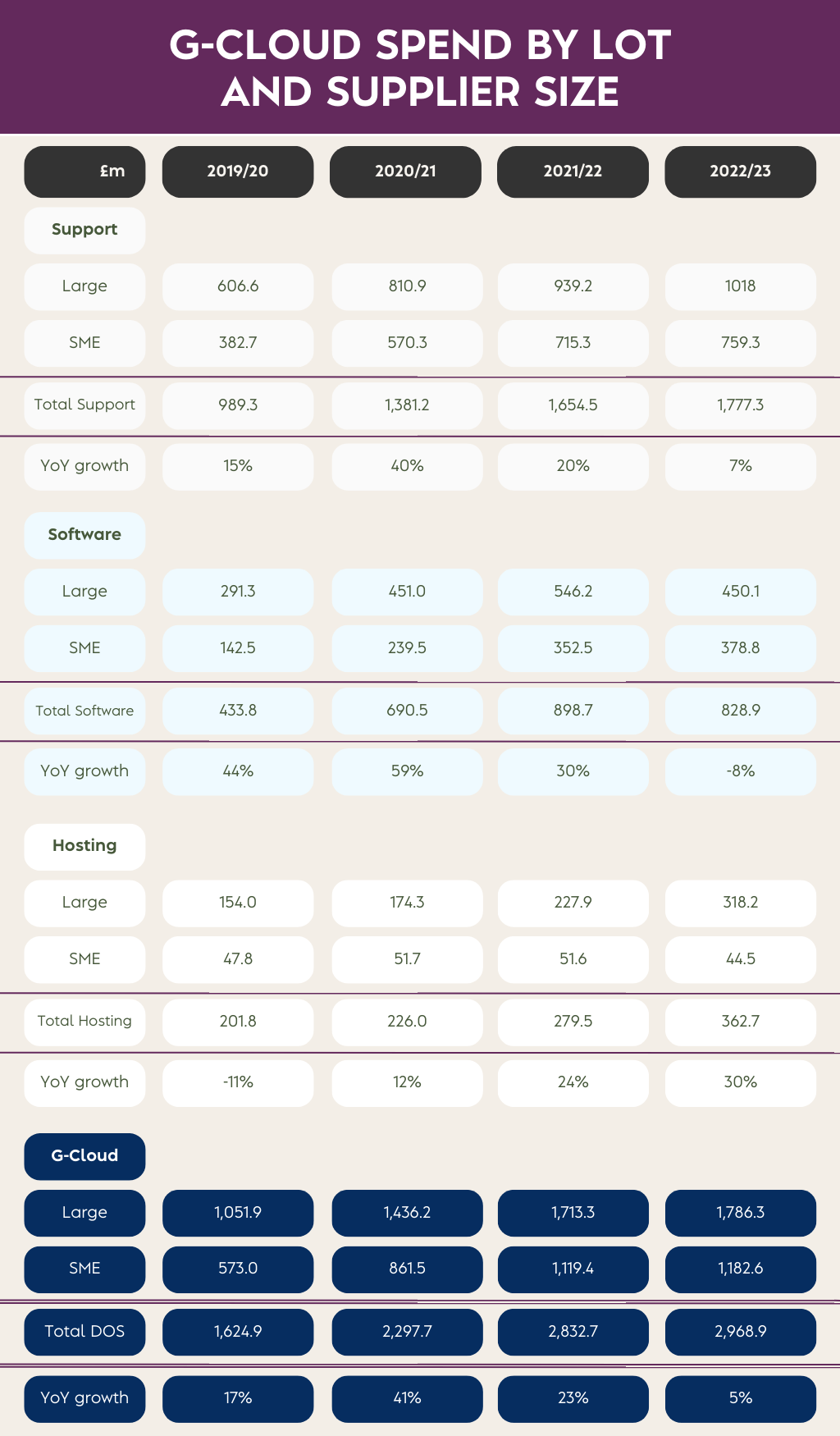

Overall spending on the Digital Marketplace continues to grow although at a lower rate (9%) than in previous years. As the Digital Marketplace is quite unique in publishing spend data (since G-Cloud commenced in 2012) we cannot see the trends for spending in other frameworks or channels that may deliver Cloud services to the public sector, so we are unable to measure what is happening to the overall demand for these services and whether this slowing of growth is a signal of saturation, lack of interest in digital transformation, financial restraint or spending simply going through other channels.

We can however drill down to see where the change is most prevalent in the Digital Marketplace. DOS has had its strongest year-on-year growth since before the pandemic, but the growth in spend to SMEs is slightly less than to Large enterprises, reversing the faster SME growth trend of the last 4-years.

The trends on G-Cloud spending in 2022/23 are markedly different from the preceding years.

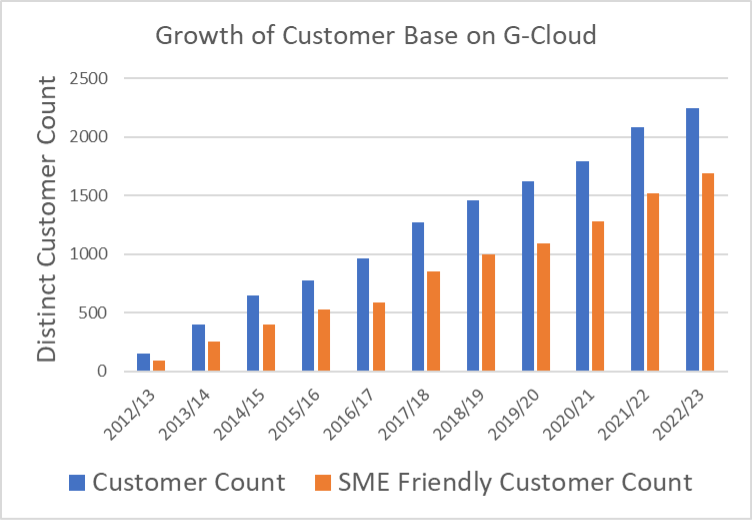

Review of Customer Base

The current (May 2023) CCS customer unique reference number list gives details of 49,000 potential customers for G-Cloud, from A1 Housing to Whipsnade Zoo. The reality is a little more manageable, in 2022/23 there were recorded 2,245 customers active in spending on G-Cloud. Of these 1,686 (75%) had at least one transaction with SMEs in the year. The growth of customers and the growth of customers willing to engage with SMEs has been positive every year of the framework’s 11-year existence.

Supply-side Dynamic

When G-Cloud 13 was launched in November 2022 there were 5,007 suppliers of which 480 were recognised as Large enterprises and 4,527 were SMEs. At commencement of the previous G-Cloud iteration (G-Cloud 12, September 2020) there were 5,057 suppliers of which 423 were Large enterprises.

The spend statistics for 2022/23 are not perfectly comparable to these supplier numbers because the spend figures include contracts arising under frameworks going back to G-Cloud 9, so when we see that 495 Large enterprises and 1,413 SMEs had made sales in 2022/23 these include some companies that are not going to be found on G-Cloud 13, for a variety of reasons. But the signal is very clear: most Large enterprises on the framework make sales, most SMEs do not. Detailed analysis I have performed (on only the Software Lot of G-Cloud 13) indicates that approximately 75% – 80% of SMEs made no sales in 2022/23. So what should an SME do, faced with this bleak statistic?

No Highway

Therefore, go forth, companion when you find No highway more, no track, all being blind, The way to go shall glimmer in the mind.

The disappointing SME performance in 2022/23 is nothing new, the ratio of successful and unsuccessful SMEs has been relatively constant since I first published “G-Cloud Success, analysed; failure explained” in 2016.

There is no quality control exercised in approving an application to get a service onto G-Cloud. An SME with a viable service in the private sector makes an application to G-Cloud and gets listed but gets no enquiries. Instead of asking ‘why?’, they accept that it’s a very different market to the one they are used to and go back to their ‘knitting’.

The problem is often that the SME doesn’t have the experience to construct the service listing on G-Cloud so that it is compliant with the procurement rules, will be capable of being found by an active buyer (there are over 30,000 services listed) and shows all the information necessary for a buyer to evaluate the service and come out on top (or in the shortlist).

So, if you are an SME with a viable product in the private sector, but your G-Cloud listing is not generating any enquiries, don’t turn away – ask ‘why?’.

Obviously, it makes sense to ask someone who knows the answer, Advice Cloud know the answer and they also know how to fix it, suppliers can make changes to their services while the framework is live: G-Cloud Buyability Assessments.

Review of the 3 components (Lots) on G-Cloud 2022/23

Professional Services

Professional Services on G-Cloud are in Lot 1 (Support) and still account for the largest part of Cloud services procured through G-Cloud at 60% of total. With DOS theoretically all comprised of Professional Services for the combined Digital Marketplace the spend on Professional Services for 2022/23 amounted to 72% of the total spend on Cloud services.

Digital Outcomes 6 (RM1043.8) is summarised on the CCS website as “A route to market to access agile development and user-centred design services to accelerate innovation within the public sector.” As such it is a ‘body-shop’ for services such as bespoke development. Whereas the rationale for G-Cloud was essentially to give public sector access to commercial off-the-shelf (“COTS”) Software-as-a-service, the infrastructure and platforms to run it on and Lot 3 (Support) was for ancillary services: “Services to help you set up and maintain your cloud software or hosting services.eg migration services or ongoing support”. G-Cloud spend on Support is more than double the spend on Software in 2022/23, which is and always has been an anomaly on G-Cloud – it is unusual for an organisation to spend twice as much on setting-up and maintaining SaaS as the cost of SaaS itself, particularly commercial off-the-shelf solutions.

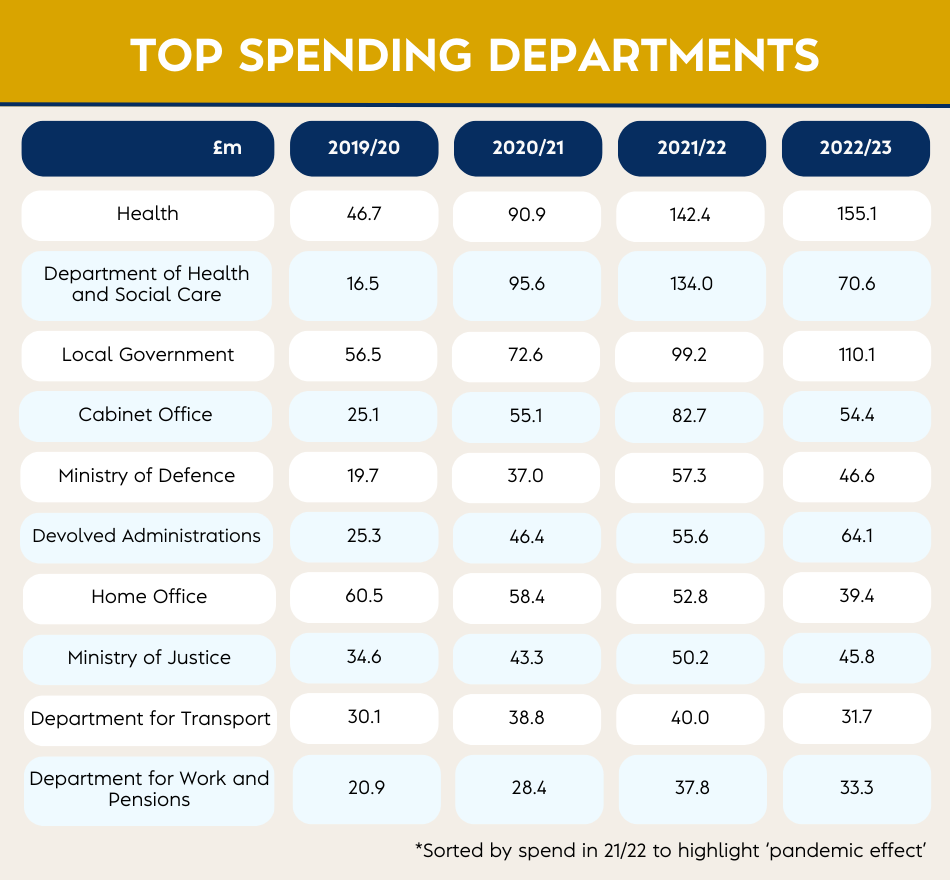

So, what is going on? One possible explanation is that compensation in the public sector has been uncompetitive for so long that it is insufficient to hire and retain talent. If a department can’t hire for a project, or even to staff ‘business-as-usual’, then there is nowhere to go but agencies and that is easier to do than addressing the root causes of the retention dilemma.

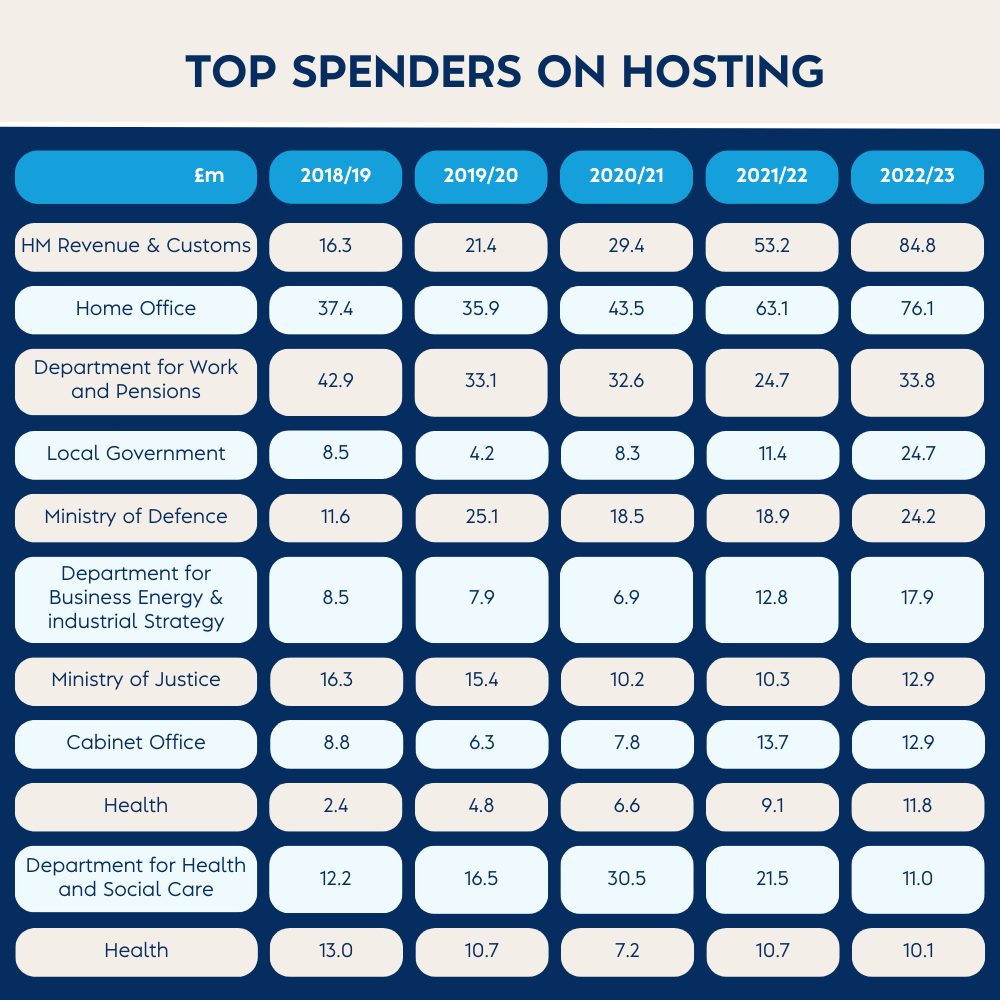

The Ministry of Defence spent less than 20% of its Support spend on SaaS in the same period.

G-Cloud Software

Spend

in 2022/23 fell by 8%. G-Cloud has been in existence for 11 financial years, starting in April 2012. This is the first year that Software spend has not increased by 30% or more over the previous financial year.

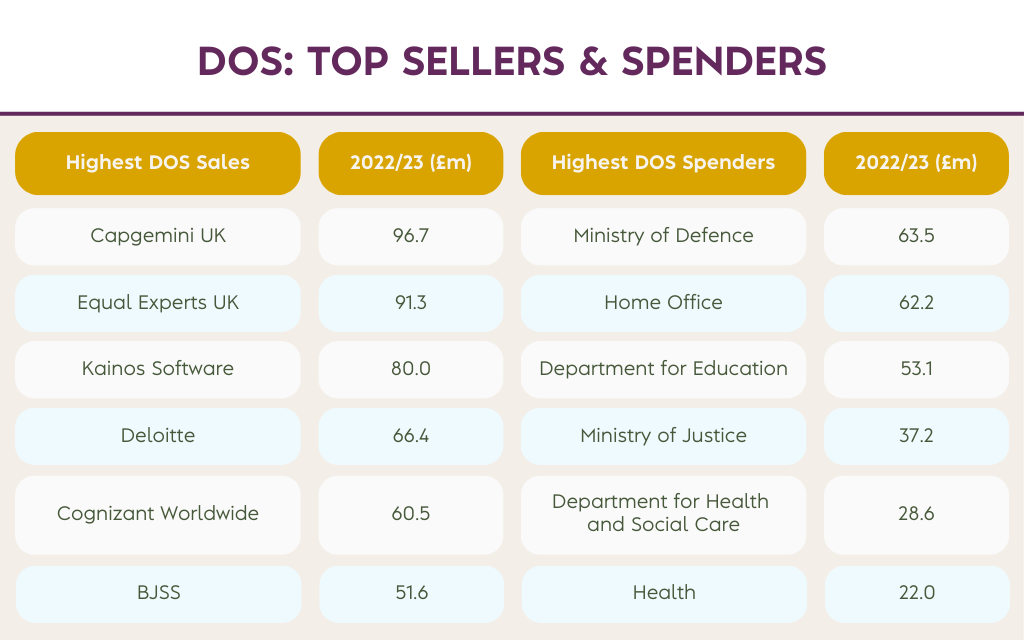

The good news is that spend on SME Software rose by 7% to about £380M although this means that Large enterprise Software sales fell by 17.5%. Part of the reason for this drop can be traced back to the emergency spending on solutions required by the response to the Covid19 pandemic. The table of top sellers below has been sorted on 2021/22 to show the bulge of spend probably attributable to this factor.

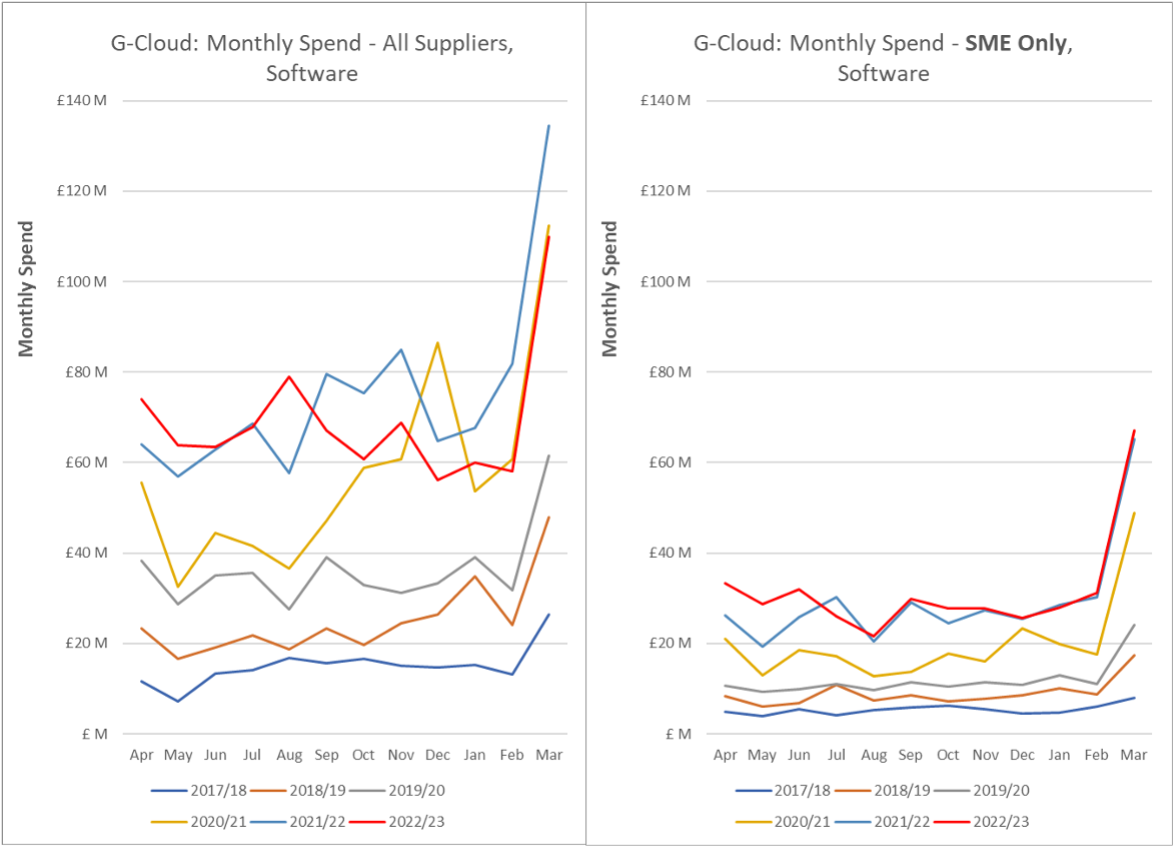

Seasonality

Seasonality is still very apparent as can be seen in the following charts of Software spend (2022/23 is the red line). Particularly in this case for the SME cohort, where ‘March Madness’ spending to use up budget was over twice the monthly average for the year.

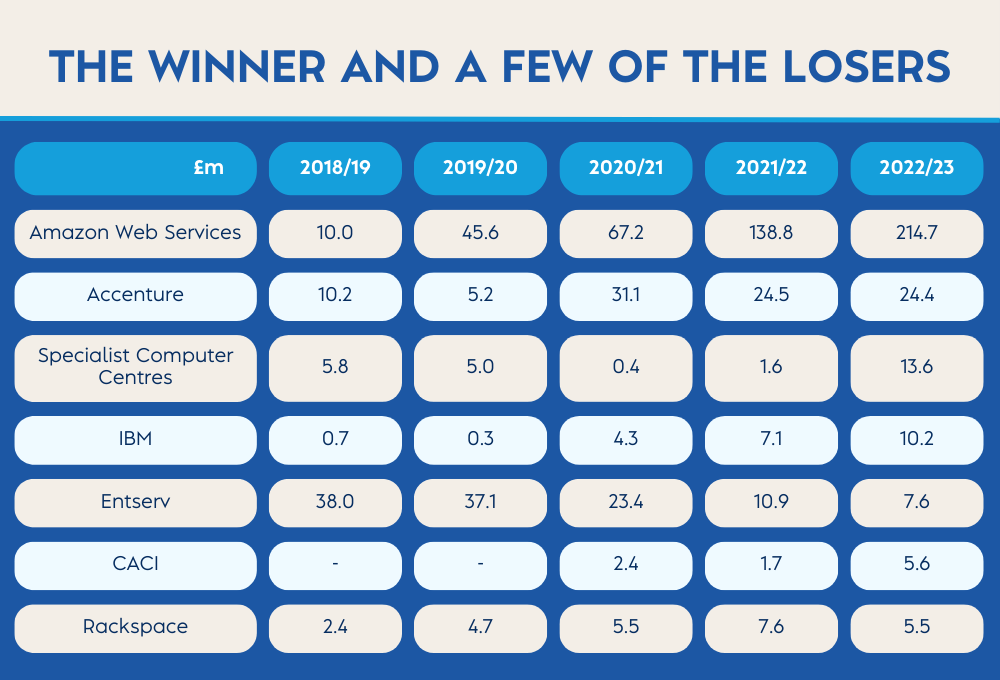

Hosting on G-Cloud

Hosting is now the tiddler of the bunch at just 12% of the total spend and with Cloud Compute 2 now open for applications, it’s quite likely that Hosting on G-Cloud will remain a small Lot.

Amazon Web Services only started on G-Cloud in 2018/19 when it achieved just under 5% market share of the Hosting Lot. It now accounts in 2022/23 for £214.7m, almost 60% of the market. The competitive battle has seen the demise of UKCloud, unable to compete against the massive capitalisation and resources of AWS, which (maybe) gave advantages in pricing, recruitment and lobbying that UKCloud could not match. So now AWS ‘owns’ the public sector hosting market – it will be interesting to see what happens to their pricing in G-Cloud 14 and whether or not our public sector turkeys have been voting for Christmas for the last couple of years.

One matter that needs to be remembered in this monopoly situation is that AWS currently price in USD$, so currency fluctuations will impact spending patterns and although recently USD/GBP has moved in favour of our domestic currency, the long term trend and my prediction for the medium term outlook is negative.