Summary

- Digital Marketplace spending in 2021 up 28%

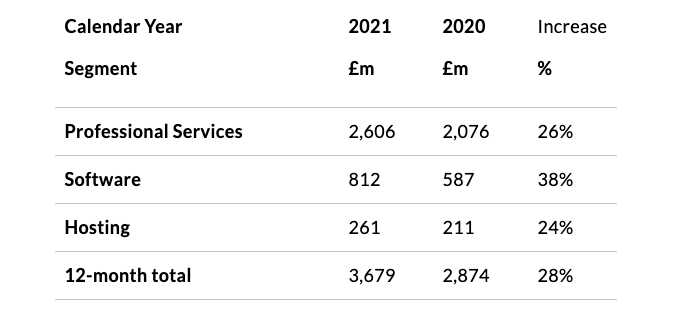

- Software highest growth Lot at 38%

- Hiatus in H1 2020 is now over, but affects comparatives

- ‘Health’ the soaraway spender at £729m (up 69% YoY)

- Professional Services a dominant 71% of spend

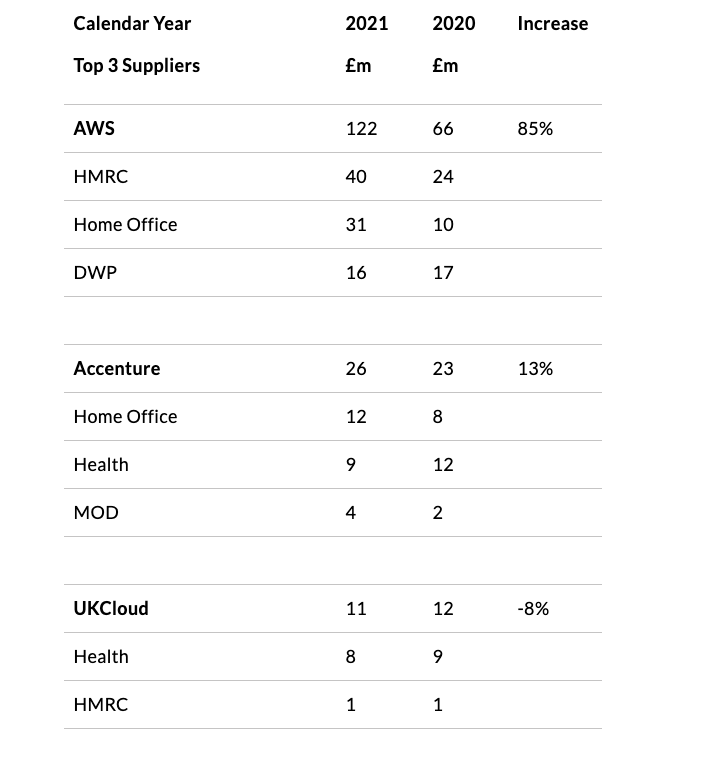

- AWS grows 85%, now owns 47% of Hosting spend

- SME spend grows in 2021, but not in Hosting

Digital Marketplace Spend Data to December 2021

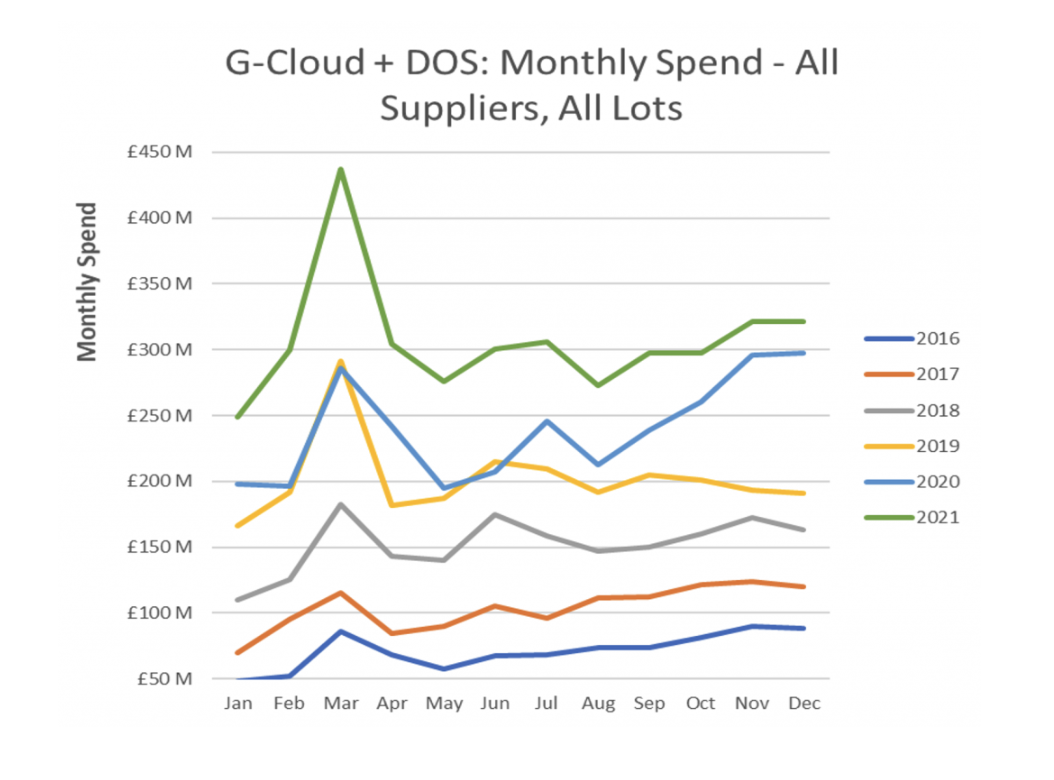

Crown Commercial Service (CCS) have published the data for spending going through G-Cloud and DOS on the Digital Marketplace up to the end of December 2021. As noted last quarter, it is important to wait for the data published in the second month after the quarter-end, because late returns often lead to significant adjustments. So, in the last review based on data released on 8th November, we ignored the October data – which has subsequently been revised upwards from £128m to £298m (132%). The September data has been revised upwards too – but only by 1%, which means we can have reasonable confidence in the data (when ignoring the last month), certainly for the purposes of this review of the ‘big picture’. Nevertheless, we can see that December Software spend on G-Cloud was comparatively low – this may be for a variety of reasons (real or inadvertent) but this is unlikely to reflect the start of a ‘trend’.

Overall, for G-Cloud and DOS combined, the strong rise in spending over the previous calendar year continued, but was very much a story of two halves. The first half achieved a 41% increase over 2020, whereas the second half increased 17% providing an overall increase of 28% for the full calendar year.

We can see a hiatus in the first half of 2020 as it scarcely grew over 2019, distorted no doubt by spending in that period being hampered by the lockdowns and other restrictions to normal activity levels starting in March 2020. Then spending in the second half of 2020 ‘caught up’ – partly as a result of spending by health increasing through the second half of 2020 and through 2021 to increase to almost triple the annual rate of spend in 2019, before the pandemic took hold.

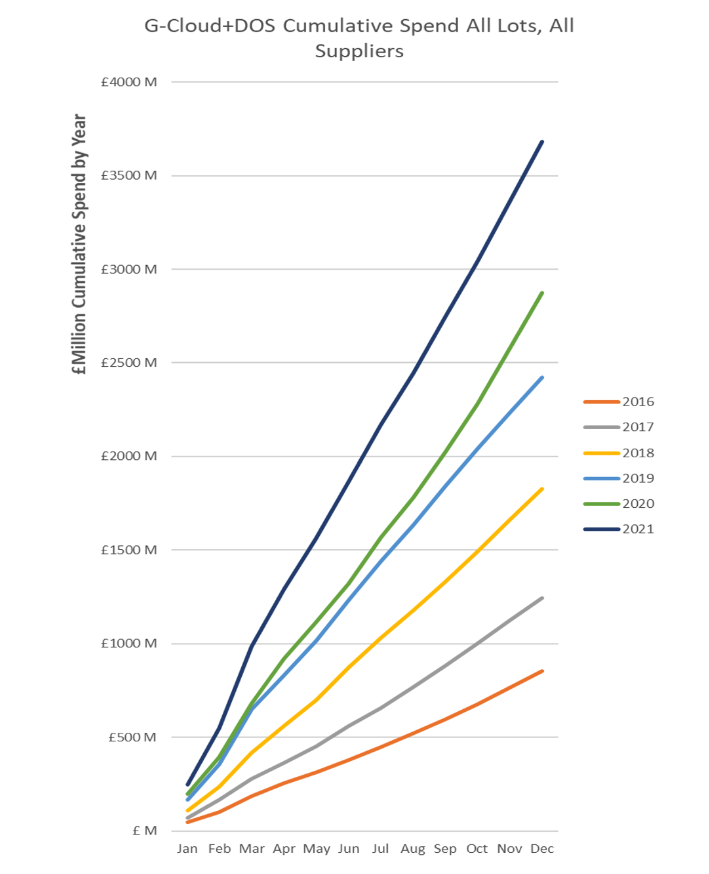

A look at the cumulative spend on G-Cloud and DOS combined (All Lots, All suppliers) shows clear evidence of strong growth of increasing Cloud adoption through these channels.

However, Digital Marketplace, while now accounting for £3.7Bn in the latest calendar year (Cf. £1.2Bn 2017) is just one channel through which Cloud spending is directed. With the increasing number of frameworks, anecdotally, we think it likely that G-Cloud and DOS are losing some ground to other channels.

Hey, Big Spender!

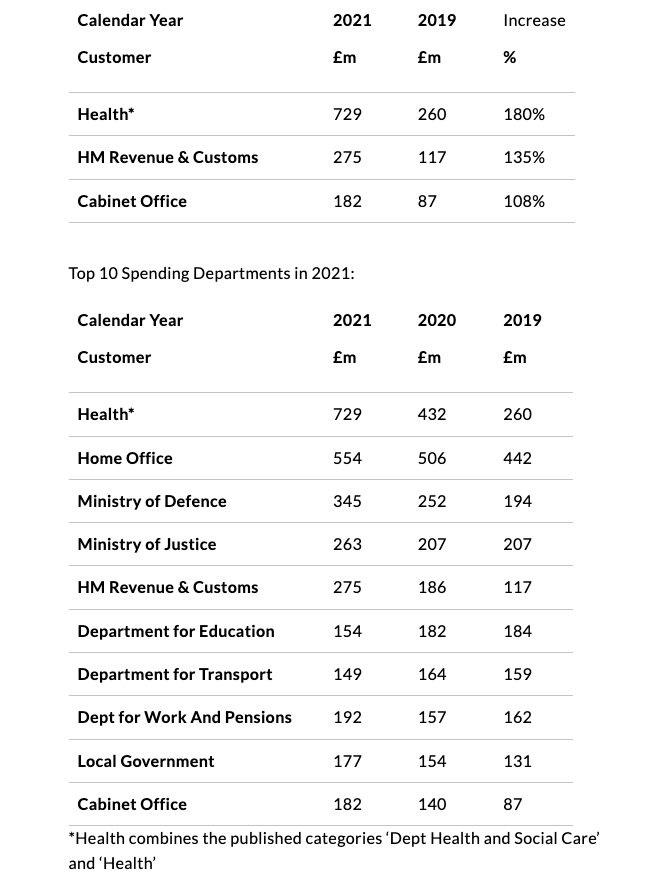

Departments spending in 2021 over 100% higher than 2019 (i.e. pre-pandemic):

Health spending to Deloitte for Software from September 2020 to December 2021 amounted to £113m. Test & Trace seems to be the main project, though whether it fits in G-Cloud Lot 2 is moot. Bespoke development is an unusual Cloud Service for inclusion in G-Cloud.

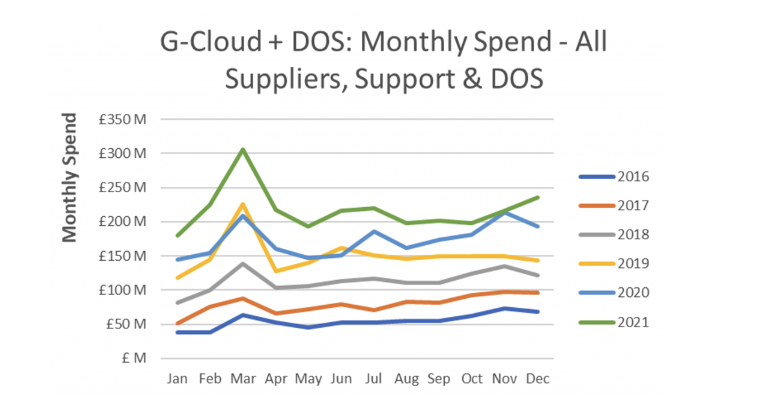

Professional Services / Support

Constituting 71% of spend on the Digital Marketplace, professional services still dominate roughly at par from 72% last year.

Looking at the chart, Professional Services (combining DOS with Lot 3 Cloud Support of G-Cloud), looks weak in the second half of 2021, but this is an illusion because of the hiatus in 2020, which, as noted above, had spending headwinds in the first half pulling the March peak to just below the 2019 comparative. Looking at the relatively flat ‘seasonality’ of spend in the previous 4-years demonstrates comparative strength of Cloud Professional Services on the Digital Marketplace in the second half of 2021.

Professional Services is perhaps less of a precisely defined category than one might think. There is an overlap with Software the size of which becomes more clear when looking at some of the big catalogue items in Software (Lot 2 of G-Cloud). When a Software supplier presents their pricing as a daily rate per person or with a disingenuously wide ‘guide price’ interval. Software is not licensed on a daily rate for a programmer, nor is it licensed as ‘we don’t know how much to charge until we’ve built it’; bespoke software development is sold that way. Should the Health spend to Deloitte be classified as Lot 2 or 3 or perhaps DOS? It is a grey area. If the software is Commercial Off the Shelf (COTS) but requires configuration (as opposed to writing new source code) arguably that’s Software spend. But I find it hard to dispute the notion that if the majority of spend is on [people x time x rate], or otherwise conditional on cost to build, then that looks more like Professional Services or a Digital Outcome.

Why might this be important? Ownership. The difference between DOS and G-Cloud is (largely) who owns the intellectual property in the outcome (be it bespoke development or derivative work). If a supplier owns the I.P. they can go on charging subscriptions until the cows come home, if the Crown owns it, they will need to spend on maintenance, enhancement and support, but they don’t pay for it over and over.

There were some additional protections in the G-Cloud 12 Call-Off Contract for Test and Trace, as a citizen tax-payer I hope NHS Digital got that one right; I can only imagine that Francis Maude, Baron Maude of Horsham, hopes so too, but I doubt that he’s holding his breath, any more than am I.

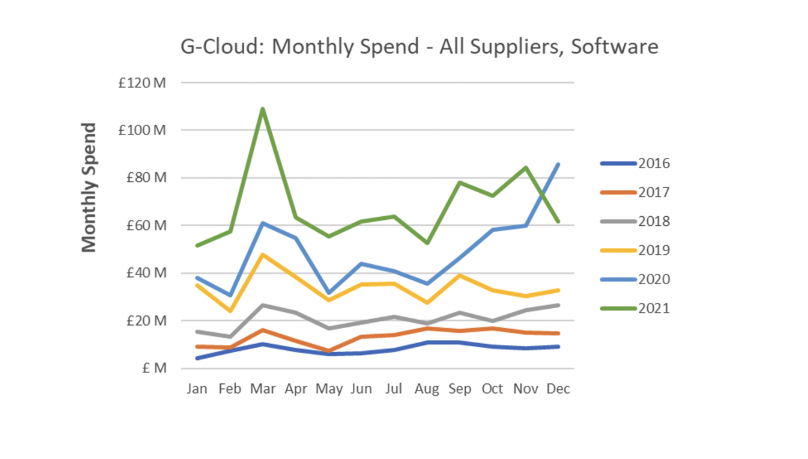

Software

Accounting for 22% of the overall spend in the marketplace in calendar 2021, Software grew by 38% to £812m.

Hosting

Cloud Hosting, which increased 24% to £261m in 2021, accounts directly for approximately 7% of spend on the Digital Marketplace, but this ignores the hosting costs bundled in Software and to some extent, Professional Services.

The top 3 Hosting vendors and their principal customers for 2021:

Size Matters

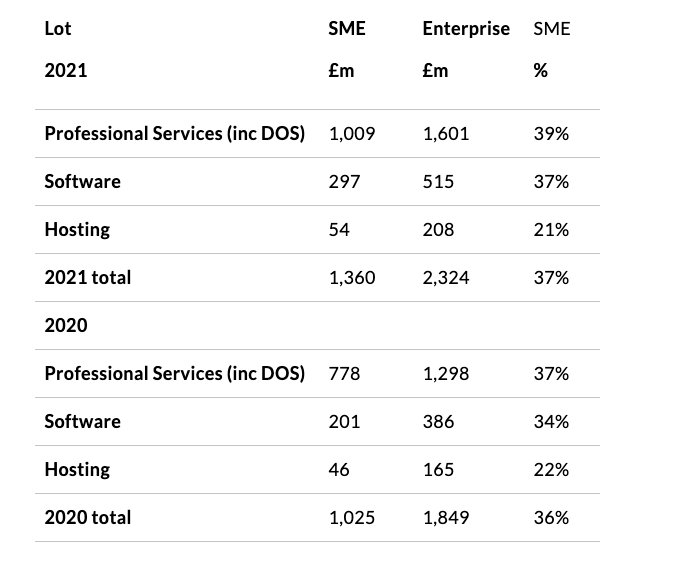

How have SMEs performed in 2021?

It is refreshing to see that the overall spend being directed towards the SME sector of the market has shown a slight increase to 37%, notably the segment going against this trend is Hosting which showed a small decline. Given the high up-front investment in physical facilities, this is a disappointing trend.

Concluding Remarks

A strong spending year on Cloud Services on the Digital Marketplace, though still heavily weighted towards Central Government. Given the squeeze on Local Government budgets it would be interesting to have a review of the progress of digital transformation across the public sector – is there a need for ‘levelling up’ in this context?

Much has been written of late concerning the contemptible briefing against UKCloud by the Cabinet Office which seems oblivious of the need to support and nurture our Tech industries. The end game of predatory pricing is a monopoly. Monopolies do not serve their customers well.

Is this another consequence of the lack of a considered Industrial Strategy directing active policy (of which public procurement is one of the biggest levers around)? Whatever the cause, the effects are predictable, reminiscent of cartoon turkeys voting for Christmas.